Accommodation Tax

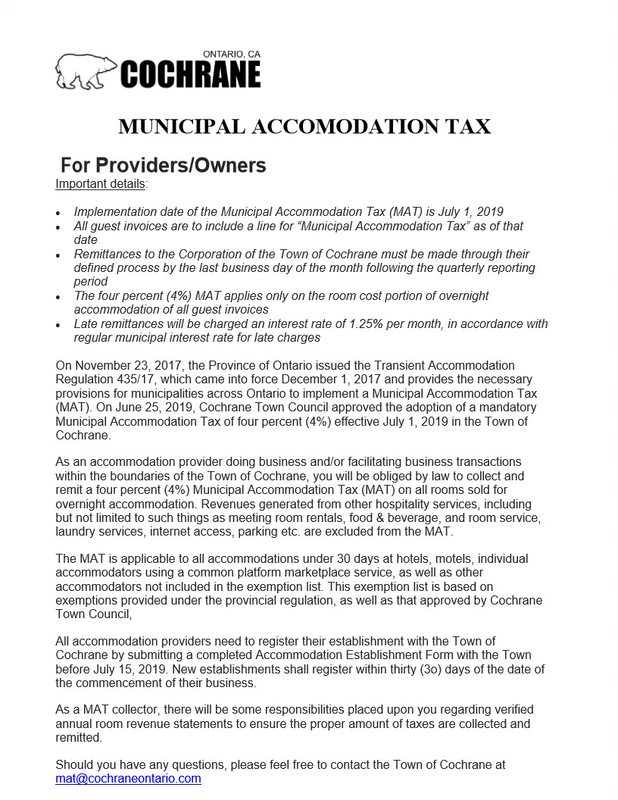

On November 23, 2017, the Province of Ontario issued the Transient Accommodation Regulation 435/17, which came into force December 1, 2017, and provides the necessary provisions for municipalities across Ontario to implement a Municipal Accommodation Tax (MAT). On June 25, 2019, the Council of the Corporation of the Town of Cochrane approved the adoption of a mandatory Municipal Accommodation Tax of four percent (4%), effective July 1, 2019, in the Town of Cochrane.

All accommodation providers doing business and/or facilitating business transactions within the boundaries of the Town of Cochrane are obliged by law to collect and remit a 4% Municipal Accommodation Tax (MAT) on all room revenue sold for overnight accommodation.

Revenues generated from other hospitality services, including but not limited to such things as meeting room rentals, food & beverage, and room service, laundry services, internet access, parking etc. are excluded from the MAT. The MAT is applicable to all accommodations under 30 days at hotels, motels, resorts, inns, individual accommodators using a common platform marketplace service, as well as other accommodators not included in the exemption list. This exemption list is based on exemptions provided under the provincial regulation, as well as that approved by Cochrane Town Council.

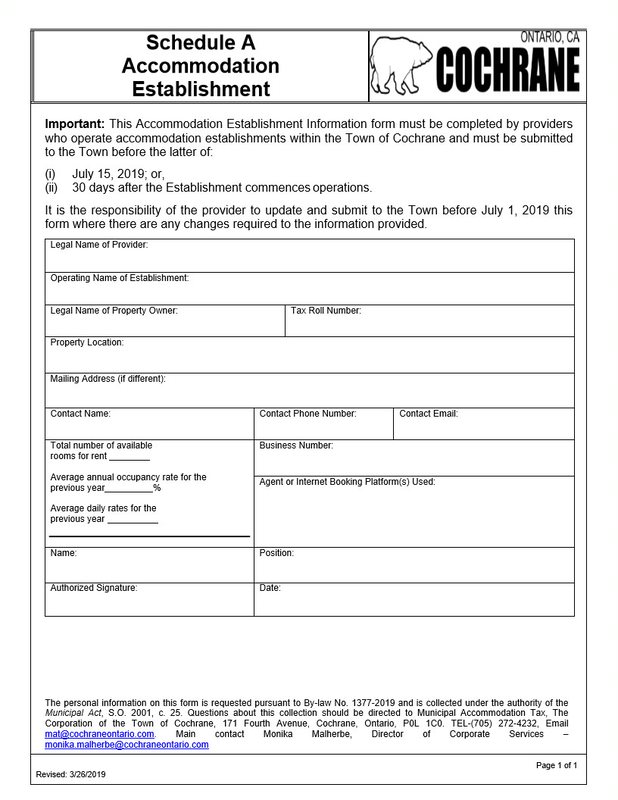

All accommodation providers need to register their establishment with the Town of Cochrane by submitting a completed Accommodation Establishment Form with the Town within thirty (30) days of the date of the commencement of their business. As a MAT collector, there will be some responsibilities placed upon you regarding verified annual room revenue statements to ensure the proper amount of taxes are collected and remitted.

The Municipal Accommodation Tax revenue will be provided, in part, to the Cochrane Tourism Association for the purposes of promoting and growing the tourism industry in Cochrane. A portion of the revenue will remain with the municipality and used to promote and grow tourism in Cochrane.

Should you have any questions, please feel free to contact the Town of Cochrane at mat@cochraneontario.com.

Information for Owners

Important details:

- The implementation date of the Municipal Accommodation Tax (MAT) is July 1, 2019

- All guest invoices are to include a line for “Municipal Accommodation Tax” as of that date

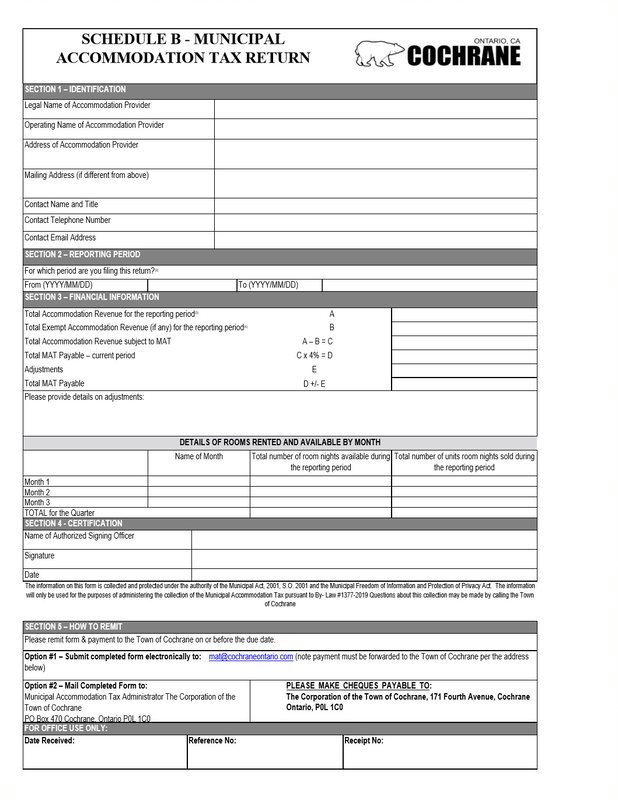

- Remittances to the Corporation of the Town of Cochrane must be made through their defined process by the last business day of the month following the quarterly reporting period

- The four percent (4%) MAT applies only on the room cost portion of overnight accommodation of all guest invoices

- Late remittances will be charged an interest rate of 1.25% per month, in accordance with regular municipal interest rate for late charges

Director Corporate Services

171 Fourth Avenue

Cochrane, ON P0L 1C0

Tel: 705-272-4361

Frequently Asked Questions

Below you will find the most frequently asked questions by providers/owners and visitors/guests.

For Providers & Owners

- Accommodations that are rented by the month 30+ days

- Lodgings provided to students by a university, college or post-secondary while the student is registered at and attending the institution.

- Every hospital referred to in the list of hospitals and their grades and classifications maintained by the minister of Health and Long-Term Care under the Public Hospitals Act and every private hospital operated under the authority of a license issued under the Private Hospitals Act

- Every long-term care home as defined in subsection 2(1) of the Long-Term Care Homes Act, 2007, retirement home and hospices

- Accommodations paid for by a School Board as defined in subsection 1 (1) of the Education Act.

- Treatment centers that receive provincial aid under the Ministry of Community and Social Services Act

- Every house of refuge, or lodging for the reformation of offenders

- Every charitable, non-profit philanthropic corporation organized as shelters for the relief of the poor or for emergency

- Every tent or trailer sites supplied by a campground, tourist camp or trailer park

Every accommodation supplied by employers to their employees in premises operated by the employer - Every hospitality room in an establishment that does not contain a bed and is used for displaying merchandise, holding meetings, or entertaining

The MAT rate is four percent (4%).

The MAT applies on the purchase price of accommodation(s) for continuous stays of 30 days or fewer. Revenues generated from ancillary services, including but not limited to such things as meeting room rentals; food and beverage; mini bar; internet; telephone; and room service will be excluded from the MAT.

All guest invoices should include a separate line for Municipal Accommodation Tax as of July 1, 2019.

If the accommodation was booked and paid in full prior to July 1, 2019, the tax will not be applicable. If it was booked before July 1, 2019 but paid on July 1, 2019 or later, the tax is applicable.

Harmonized Sales Tax (HST) is applicable to the MAT.

The MAT is mandatory pursuant to Town of Cochrane Bylaw 1377-2019

Providers will use the remittance form and instructions to file their MAT return for the quarterly reporting periods.

January 1 – March 31: Due April 30

April 1 – June 30: Due July 31

July 1 – September 30: Due October 31

October 1 – December 31: Due January 31

Where the deadline falls on a Saturday, Sunday or holiday, the deadline shall be the last business day of the month in which the remittance is due.

Payments must be made by way of cheque payable to The Corporation of the Town of Cochrane at the same time as the remittance form is due. Other options for payment such as EFT and electronic filings will be explored at a later date.

Payment of the MAT is not to be included with any other payments, such as property taxes.

Providers may submit their remittance form with payment by mail to:

Corporation of the Town of Cochrane

171 Fourth Avenue

Cochrane, Ontario

P0L 1C0

Alternatively providers are able to email their remittance form to mat@cochraneontario.com on or before the due date. Payment by way of Cheque will still be required to be delivered to the address noted above.

If the accommodation was booked and paid in full prior to July 1, 2019, the tax will not be applicable. If the accommodation was booked before July 1, 2019 but paid in part or in full on July 1, 2019 or later, the full MAT will be applied to the purchase price of the accommodation.

The MAT will support important Town of Cochrane tourism programs and contribute to a strong and vital community. One half of the net MAT revenue will be shared with the Cochrane Tourism Association (CTA) to support their promotion and development of Cochrane tourism. The other 50% of net MAT revenue will remain with the Town to provide funding for future project/initiatives which aim to support tourism.

If the Municipal Accommodation Tax was added to an invoice which was paid by a guest, and you subsequently issue a full or partial refund on that accommodation charge, the customer should also be refunded the applicable amount of MAT that corresponds to the refund amount. If the refund occurs after you have remitted the MAT, you can adjust the MAT submission the following month noting the refund in your submission documentation.

If you experience no shows and your policy is to charge a portion of the room rental as a penalty, then the MAT should also be charged to the no show portion.

Yes, you will need to file a MAT remittance for each reporting period regardless of whether there was any MAT charged and collected.

Yes, providers will be required to provide upon request documents necessary to support the information on their MAT remittances.

The Town or a third party designate shall be granted access to enter the business premises for the purpose of inspecting documents to ensure compliance with its by-law and will have the authority to audit and request information from any provider, including:

- Audit or examine the books and records that relate to the amounts payable to the Town; and

- Require a provider to produce all documents required by the Town for an audit and to answer all questions relating to the audit and give all reasonable assistance with the audit.

Pursuant to Town of Cochrane Bylaw 1377-2019. This bylaw is pursuant to Ontario Regulation 435/17.

Revenues generated from ancillary services, including but not limited to such things as meeting room rentals; food and beverage; mini bar; internet; telephone; and room service will be excluded from the MAT provided they are itemized separately on the invoice.

Harmonized Sales Tax (HST) is applicable to the MAT.

Not necessarily, the MAT is applicable only to the purchase price of accommodation.

Interest and penalties will apply on any overdue remittance as follows:

- Penalty calculated as 25% on the amount of any Municipal Accommodation Tax (MAT) due and owing on the first day of default; and

- Interest calculated as 1.25% per month on the amount of any MAT due and owing from the first day of each month subsequent to the date of default up to and including the month in which the tax is paid in

Failure to file and remit as required may result in MAT assessments imposed by the Treasurer. Interest and penalty will apply once amounts are determined.

Please email inquiries to mat@cochraneontario.com

All guest invoices should include a separate line for MAT as of July 1, 2019.

No the revenue used to determine the MAT is the gross purchase price of the accommodation. Costs incurred by the provider to secure the accommodation are not deductible against the MAT revenue base.

The party responsible for providing the accommodation is also responsible for the collection and remittance of the MAT.

No, the entire stay is exempt from the MAT.

The MAT must be charged starting July 1, 2019 only.

The MAT is not applied to any nights prior to July 1, 2019.

Yes, if the final payment for a room occurs on or after July 1, 2019 the MAT applies to the accommodations rate regardless of any deposits made.

No, indigenous peoples are not exempt from paying the MAT.

Funds generated through the Municipal Accommodation Tax are invested in sales, marketing, and development activities through Cochrane Tourism, the town’s official destination marketing organization. Cochrane Tourism promotes Cochrane for leisure visitors, meetings and conventions, major events, media relations, tour operators, and travel trade. Cochrane Tourism also invests in long term destination development initiatives aimed at enhancing the visitor experience.

Municipal Accommodation Tax participants are entitled to complimentary membership with Cochrane Tourism, and have opportunities to become directly involved in various committees that guide the planning and budgeting of the organization.

If the Municipal Accommodation Tax was added to an invoice that was paid by a guest, and you subsequently issue a full or partial refund on that accommodation charge, the customer should also be refunded the applicable amount of MAT that corresponds to the refund amount. If the refund occurs after you have remitted the MAT, you can adjust the MAT submission the following month noting the refund in your submission documentation.

If you experience no shows and your policy is to charge a portion of the room rental as a penalty, then the MAT should also be charged to the no show portion. If, however, you have a flat administrative fee that is charged for no shows no matter what the room rate, then the MAT does not need to be applied.

Yes, if all of your guests were for extended stay (30 days or longer) or another qualified exemption you must still submit a monthly report providing the details for the exception.

For Visitors & Guests

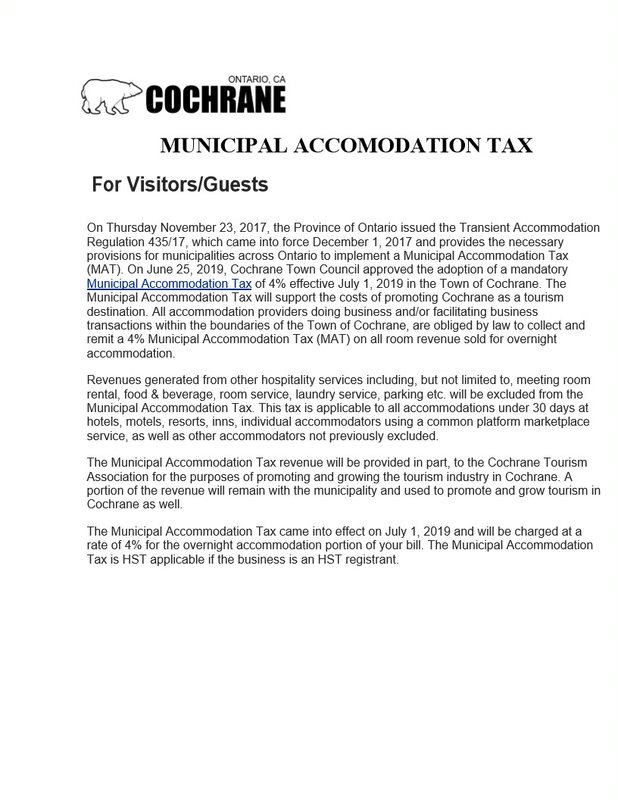

The MAT rate is four percent (4%).

The MAT applies on the purchase price of accommodation(s) for continuous stays of 30 days or fewer. Revenues generated from ancillary services, including but not limited to such things as meeting room rentals; food and beverage; mini bar; internet; telephone; and room service will be excluded from the MAT.

All guest invoices should include a separate line for Municipal Accommodation Tax as of July 1, 2019.

If the accommodation was booked and paid in full prior to July 1, 2019, the tax will not be applicable. If it was booked before July 1, 2019 but paid on July 1, 2019 or later, the tax is applicable.

Harmonized Sales Tax (HST) is applicable to the MAT.

Yes, the MAT will apply to this type of accommodation for continuous stays of 30 days or fewer.

No, the MAT is a mandatory tax on the purchase price of accommodation for continuous stays of 30 days or fewer.

The MAT will support important Town of Cochrane tourism programs and contribute to a strong and vital community. One half of the net MAT revenue will be shared with the Cochrane Tourism Association (CTA) to support their promotion and development of Cochrane tourism. The other 50% of net MAT revenue will remain with the Town to provide funding for future project/initiatives which aim to support tourism.

Toggle If you are charged for the accommodation, whether or not you actually occupy it or not, then MAT will apply. If you do not cancel your room reservation and you are charged for accommodation (no-show included), the MAT will be charged. If you are not charged for the accommodation but subject to a cancellation fee, the MAT should not apply.

{kind=link}

{kind=link}

{kind=link}

{kind=link}